On June 11, 2021, the Federal Budget for FY 2021-2022 was announced, with an outlay of 8.4 trillion rupees and a forecasted real GDP growth of 4.8%. After a three year period of tough macro-economic stabilisation processes, the government is keen to carry the growth momentum forward. Traditionally, it has used the Public Sector Development Program (PSDP) as an important driver to fuel growth.

Set at Rs 900 billion (10.6% of the outlay) for the forthcoming fiscal year, there has been an increase of Rs 270 billion from the outgoing fiscal year. In FY 2017-2018, when the PSDP was set at one trillion rupees, of which only 66% could be utilised, the previous government was able to achieve a real GDP growth of 5.5%.

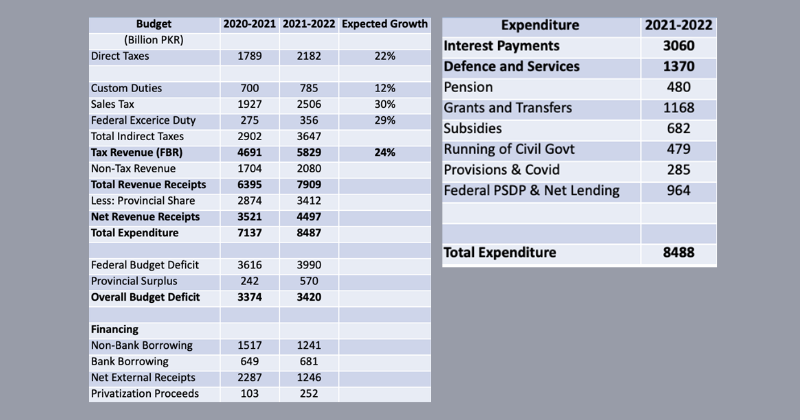

On the revenue front, the FBR has set a target of Rs 5.8 trillion for FY 2022, compared to Rs 4.7 trillion for the outgoing year. Given the forecasted real GDP growth, coupled with an expected eight percent inflation rate, a nominal GDP growth of 12.8% is expected. This would imply that tax revenues will increase to Rs 5.3 trillion, with the economy expanding, and the government intending to collect an additional Rs 506 billion through taxation and enforcement measures. The proposed taxation amounts to Rs 383 billion, which include a 17% sales tax on crude oil, silver/gold jewellery, a 7.5% withholding tax on electricity bills above Rs 25,000 for domestic users not appearing on the active taxpayers list and a sales tax on sugar retail prices and the withdrawal of several tax exemptions.

On the non-tax revenue front, an important driver of revenue has been Petroleum Development Levy (PDL) on the accumulated price of oil (ex-refinery/import price, inland freight margin, oil marketing companies, dealers and distribution commission and GST) by the government. For the outgoing fiscal year, PDL was budgeted at Rs 450 billion, which seemed unattainable. However, a decline in global oil prices benefitted the government, which managed to collect Rs 369 billion for the period July-March 2021. Crude oil prices have since witnessed a bull run with Brent currently standing at $73 per barrel today and PDL has declined to Rs 4.8 for Petrol and Rs 5.1 per litre for HSD, compared to RS 25-30 per litre a couple of months ago. Despite the fact that a limited cushion is left in PDL, the government has budgeted Rs 610 billion for FY 2022, a 35% increase over the last year’s target. The government is relying on oil prices to decline in the future once sanctions from Iran are lifted and an oil credit facility from Saudi Arabia is received, allowing it to generate the targeted PDL without having to increase prices. However, if these assumptions deviate, we can expect an increase of Rs 20-25 per litre in petrol and diesel prices.

In FY 2011, Pakistan had a tax to GDP ratio of 9.3%, which after a decade is estimated to stand at 12.7%, a marginal increase of 0.3% per year. A low tax to GDP ratio leaves the fiscal position vulnerable and increases the debt burden, which continues to eat a big portion of the cake. If, assuming, the revenue targets are met, the government intends to collect Rs 7.9 trillion in tax and non-tax revenue, of which Rs 3.4 trillion will be transferred to the provinces, leaving the Federal government with Rs 4.49 trillion. This is only sufficient to pay debt servicing costs of Rs 3.06 trillion (Rs 1.36 trillion in FY 2018) and defence services, which stand at Rs 1.37 trillion (Rs 920 billion in FY 2018), and the rest of the expenditures will come from borrowed money, adding to the debt burden.

To ensure fiscal sustainability and build resilience, there is an imminent need to increase the tax to GDP ratio by three to four percent over the next few years to match the increase in expenditures. The World Bank estimates that using a broad-based low rate approach without imposing new taxes and other necessary measures, the tax to GDP ratio can be increased to 26% (the UK is currently at 25%).

In the FBR’s biannual review, a recent study showed the impact of the services sector on Pakistan’s economic growth and tax revenues. The services sector has become a major contributor to the economy, with its share to GDP standing at 61%. Over the past few years, the wholesale and retail trade has grown tremendously and currently accounts for 18.82% of the GDP. The services sector combined now contributes 26% to Pakistan’s tax revenue. Analysis shows that there are some structural factors that do not allow the contribution from this sector to increase beyond this mark.

There are several issues. A good portion of this sector still remains undocumented and cash transactions are standard practice. Additionally, these are uneducated ownerships, lack of capital, undocumented dealings and shipments. One can still buy relatively pricier items, such as laptops, phones, air conditioners and other goods with cash, which is unaccounted for and is not get added to the government’s tax collection. Furthermore, according to SDPI, companies are not registering with FBR because they believe this will hold back growth. Businesses are afraid of intrusion, cost of compliance and lack of understanding on tax matters. It is important to remove these bottlenecks, implement information technology, educate workers and create awareness to increase documentation.

To mobilise and achieve these revenue targets, the government has rolled out a plan to extend the use of Point of Sale (POS) to 500,000 users, particularly for large wholesale and retail markets. However, the difficulty lies in the implementation. As per the FBR, registered POS currently stand at 11,000 users and only generated Rs 14 billion.

Based on current expectations, tax revenue targets could see a shortfall of Rs 150 to 200 billion and the PDL target is already quiet ambitious. These shortfalls could result in the government slashing PSDP, subsidies and provincial distribution. The problem remains. The low tax to GDP ratio and the undocumented economy (which according to Bloomberg accounts for 36% of the overall economy) will keep the fiscal position vulnerable and this macroeconomic instability impedes sustainable economic growth.

In current times, when global economies are relying on fiscal flexibility to support healthcare, households and economic recovery, our targets are still to contain the fiscal deficit. This stems from the reluctance to switch to documented transactions and unless reformative and corrective measures are implemented, the government will again find itself with an ever increasing debt burden and little room for fiscal easing.

Ali Jamshed is a lecturer for undergraduate Accounting and Finance courses and an A-Level Accounting teacher with research interests in economic policy and financial sector management.

Comments (0) Closed